A major shift in U.S. retirement policy is underway. President Donald Trump has signed a new executive order aimed at expanding access to retirement savings for millions of American workers who currently lack employer-sponsored plans.

The move targets a long-standing gap in the U.S. financial system, where tens of millions of workers—especially low-income earners, freelancers, and small-business employees—do not have access to traditional retirement accounts such as 401(k)s.

The executive order aims to expand retirement access to millions of Americans

What the Executive Order Does

The new policy directs the U.S. Treasury Department to create a centralized platform, expected to be launched as TrumpIRA.gov, where workers can browse and enroll in private retirement plans. :contentReference[oaicite:0]{index=0}

This system is designed to simplify access by allowing individuals to compare plans based on cost, investment options, and requirements. :contentReference[oaicite:1]{index=1}

Importantly, the initiative focuses on workers who do not receive retirement benefits through their employers—a group estimated at around 50 to 56 million Americans. :contentReference[oaicite:2]{index=2}

How the “Saver’s Match” Works

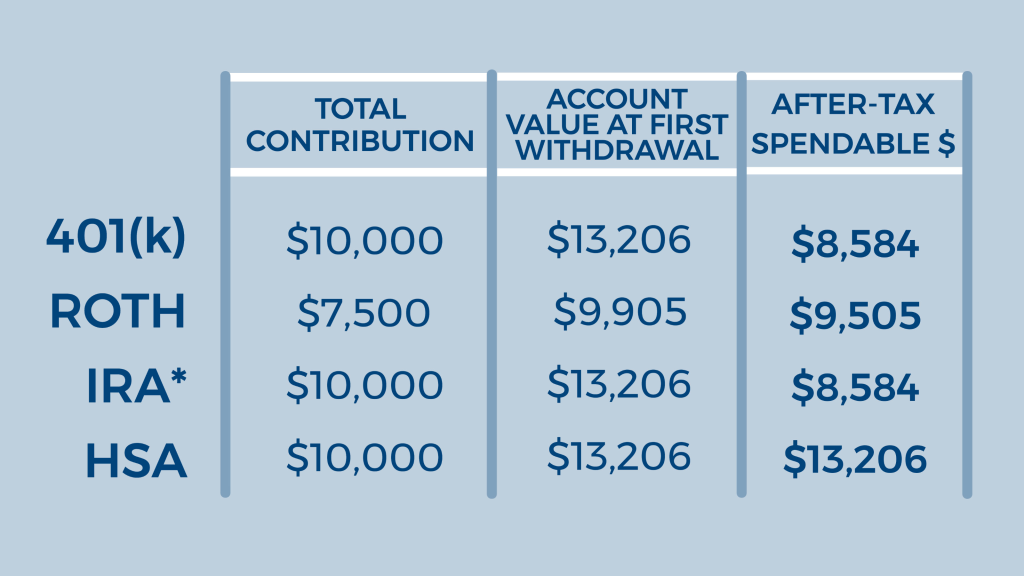

A key component of the plan is the expansion of the Saver’s Match program. Starting in 2027, eligible low-income workers will receive a federal match of up to $1,000 annually for their retirement contributions. :contentReference[oaicite:3]{index=3}

This builds on earlier legislation, transforming what was previously a tax credit into a direct government contribution deposited into retirement accounts.

As a result, the program aims to encourage participation among workers who previously had little incentive—or ability—to save for retirement.

The Saver’s Match could boost retirement savings for low-income workers

Why This Matters

The executive order addresses a critical issue: nearly half of private-sector workers in the U.S. lack access to employer-sponsored retirement plans. :contentReference[oaicite:4]{index=4}

Consequently, millions of Americans face the risk of inadequate savings in retirement. By expanding access, the administration hopes to close this gap and improve long-term financial security.

Did You Know? Experts say this could be one of the largest expansions of retirement coverage since Social Security. :contentReference[oaicite:5]{index=5}

Who Benefits the Most?

The policy is particularly targeted at underserved groups, including:

- Gig workers and freelancers

- Employees of small businesses

- Low- and middle-income earners

- Workers without 401(k) access

For these groups, the combination of easier enrollment and government matching contributions could significantly improve retirement outcomes.

Strengths of the Policy

- Expanded Access: Millions more workers can now participate in retirement savings

- Government Incentives: The Saver’s Match boosts contributions

- Private-Sector Flexibility: Workers can choose from multiple IRA providers

Additionally, the platform model allows portability, meaning workers can keep their accounts even if they change jobs.

Criticism and Limitations

Despite its potential, the executive order has limitations. Critics argue that access alone may not be enough, especially for low-income workers who struggle to save.

Moreover, some experts emphasize that stronger reforms—such as automatic enrollment or higher matching contributions—would require congressional approval.

There are also concerns about whether voluntary participation will achieve widespread adoption without additional incentives.

Experts say access alone may not solve long-term retirement challenges

Political and Economic Impact

Politically, the move has drawn bipartisan attention, with some analysts calling it a “game changer” for retirement access.

Economically, the initiative could increase investment flows into financial markets, as more Americans begin saving through IRAs and similar accounts.

However, its long-term success will depend on participation rates and whether Congress expands the program further.

President Trump’s executive order represents a significant step toward expanding retirement access in the United States. By targeting millions of workers without employer-sponsored plans, the policy aims to close a major gap in the financial system.

Key takeaway: While the initiative has strong potential, its real impact will depend on how many Americans take advantage of the new opportunities—and whether additional reforms follow.

Frequently Asked Questions

1. What is the purpose of the executive order?

It aims to expand access to retirement savings for workers without employer-sponsored plans.

2. What is TrumpIRA.gov?

It is a planned platform where workers can compare and enroll in retirement accounts.

3. Who qualifies for the Saver’s Match?

Low-income workers earning below certain thresholds can receive up to $1,000 in matching contributions.

4. When will the program start?

The Saver’s Match is expected to begin in 2027.

5. How many people could benefit?

Approximately 50–56 million Americans without retirement plans.

6. Does this replace 401(k) plans?

No, it complements existing plans by targeting workers who lack access.

{kind=link}