In 2026, stablecoins have emerged as a transformative force in global finance. These digital assets, designed to maintain a stable value pegged to the U.S. dollar or other reserves, are increasingly integrated into everyday financial operations. For U.S. banks, this represents a pivotal moment of disruption and adaptation following landmark regulatory developments.

What Are Stablecoins and How Do They Work?

Stablecoins are cryptocurrencies engineered for price stability, typically backed 1:1 by reserves such as cash, U.S. Treasuries, or other high-quality assets. Unlike volatile cryptocurrencies like Bitcoin, major players like Tether (USDT) and Circle’s USDC offer reliability that appeals to institutions and retail users alike.

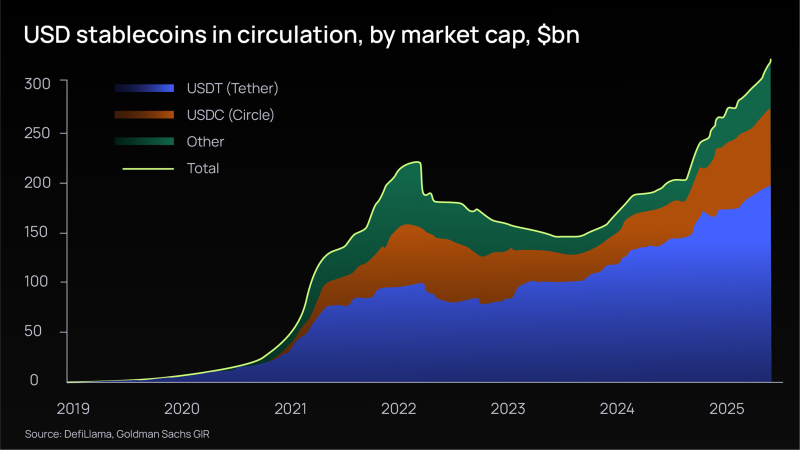

They operate on blockchain networks, enabling near-instant, 24/7 settlement with minimal fees compared to traditional systems like ACH or SWIFT. In 2026, fiat-backed stablecoins dominate, accounting for over 99% of the market, with USDT and USDC leading in market capitalization and liquidity.

Stablecoin market capitalization has grown rapidly, with projections approaching $1 trillion by late 2026.

The GENIUS Act: Regulatory Clarity Accelerates Adoption

The enactment of the GENIUS Act in mid-2025 marked a turning point. This legislation establishes a federal framework for payment stablecoins, requiring robust reserves, transparency, and compliance with anti-money laundering standards. Federal agencies including the OCC, FDIC, and Federal Reserve are finalizing implementing rules throughout 2026.

This clarity has legitimized stablecoins, encouraging banks and non-banks to participate. OCC approvals for national trust bank charters for crypto firms and proposed rules on issuance have opened doors for innovation while addressing systemic risks.

How Stablecoins Are Disrupting Traditional Banking Models

Impact on Deposits and Funding

One of the primary concerns for U.S. banks is deposit flight. Estimates suggest trillions in bank deposits could migrate to stablecoins as users seek faster yields or programmable money. The American Bankers Association has highlighted risks to lending, particularly for community banks.

Stablecoin issuers hold reserves primarily in Treasuries and bank deposits, but the shift reduces low-cost funding sources for traditional lending. Banks may face higher costs of funds and pressure on net interest margins.

Payments and Cross-Border Transactions

Stablecoins excel in efficiency. Transactions settle in seconds for fractions of a cent, compared to days and higher fees in legacy systems. Businesses use them for remittances, supply chain payments, and treasury operations, bypassing correspondent banking networks.

In 2026, stablecoins processed tens of trillions in on-chain volume. Partnerships between Visa, Mastercard, and stablecoin platforms signal mainstream integration, potentially eroding banks’ payment fee revenues.

Competition from Non-Banks and Fintechs

Fintech companies and new issuers are moving faster than incumbents. While some large banks explore their own stablecoins or tokenized deposits, non-banks dominate issuance. This creates a parallel financial ecosystem that challenges banks’ intermediary role.

Opportunities for U.S. Banks in the Stablecoin Era

Forward-thinking banks are not just defending but innovating. Strategies include:

- Issuing or partnering on stablecoins for custody, on/off-ramps, and settlement.

- Integrating blockchain for internal efficiencies and client services.

- Offering tokenized deposits that combine bank backing with digital speed.

- Expanding into related services like crypto custody and compliance tools.

Major institutions like JPMorgan, Bank of America, and others are involved in consortium efforts or pilots. Banks with strong compliance infrastructures are well-positioned to capture new revenue streams.

U.S. banks are increasingly partnering with fintechs to integrate stablecoin capabilities.

Risks and Challenges for 2026 and Beyond

Financial stability remains a key focus. Rapid growth could concentrate reserves, amplify runs during stress, or transmit shocks across systems. Regulators emphasize 1:1 reserves, redemption capabilities, and AML controls.

Banks must navigate yield debates—whether stablecoins can offer interest-like returns without undermining deposit bases—and evolving international standards.

Real-World Examples and Case Studies

Circle and Tether continue to expand use cases in emerging markets for remittances. In the U.S., pilots with payment networks demonstrate instant settlement benefits. Corporate treasurers report significant cost savings on cross-border flows.

Lead Bank and other institutions facilitate accounts for crypto apps, bridging traditional and digital rails. These examples illustrate both disruption and symbiotic growth.

What 2026 Means for U.S. Banks: Strategic Imperatives

Banks that treat stablecoins as a strategic priority—investing in technology, talent, and partnerships—will thrive. Those slow to adapt risk losing market share in payments and client relationships.

The year ahead will see further rulemaking, increased issuance under the GENIUS framework, and deeper integration with traditional infrastructure. Stablecoins are not replacing banks entirely but forcing evolution toward a hybrid, more efficient financial system.

Frequently Asked Questions

What are stablecoins and why are they disrupting banking?

Stablecoins are digital dollars backed by reserves, offering fast, low-cost transactions on blockchain. They disrupt by providing alternatives to slow, expensive traditional payments and deposits.

How does the GENIUS Act affect U.S. banks?

The Act provides regulatory clarity for stablecoin issuance, enabling banks to participate while imposing standards on reserves and compliance, reshaping competition in 2026.

Will stablecoins replace bank deposits?

Not entirely, but significant migration is possible. Banks are responding with tokenized offerings and partnerships to retain funding and serve client demand for digital assets.

What are the main risks of stablecoins for the banking system?

Key risks include deposit outflows, liquidity concentration, potential runs, and systemic interconnections. Strong regulation aims to mitigate these.

How can banks benefit from stablecoins in 2026?

Banks can issue stablecoins, provide custody, facilitate settlements, and develop new services, creating revenue opportunities in a growing digital economy.

Which stablecoins are most prominent in 2026?

USDT (Tether) and USDC (Circle) lead the market, together dominating supply and transaction volume due to liquidity and regulatory compliance.

{kind=link}