Embedded finance has evolved from a fintech innovation into a core strategy for banks and platforms alike. By 2026, it enables financial services to appear naturally within the apps and journeys customers already use daily.

What Is Embedded Finance?

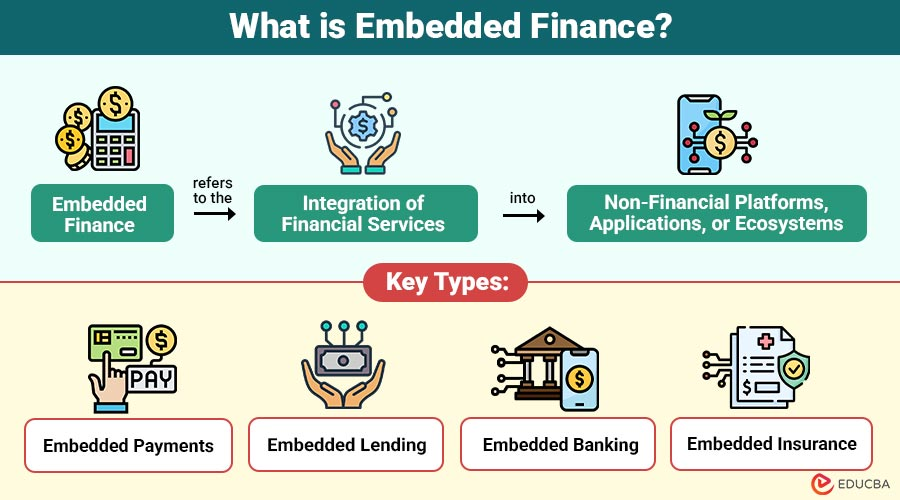

Embedded finance is the integration of financial products—such as payments, lending, insurance, deposits, and banking services—directly into non-financial software platforms and customer experiences. Instead of redirecting users to a bank app or website, these services are offered seamlessly at the point of need.

Platforms act as distributors while banks or Banking-as-a-Service (BaaS) providers handle the regulated backend. This creates “invisible banking” where finance supports the primary activity without friction.

Embedded finance integrates banking services directly into everyday platforms and life events.

Life-Moment Banking: Contextual Finance at Key Times

Life-moment banking refers to delivering targeted financial solutions precisely when customers face significant events—buying a home, starting a business, paying for education, or managing unexpected expenses. In 2026, banks use data, APIs, and partnerships to anticipate and serve these moments within partner ecosystems.

Examples include instant auto loans during online car shopping or embedded payroll advances in HR software. This proactive, contextual approach boosts relevance and customer loyalty.

How Banks Are Implementing Embedded Finance in 2026

Embedded Payments and Commerce

Banks partner with e-commerce and SaaS platforms to embed checkout, invoicing, and B2B payments. This reduces friction and captures revenue through interchange and fees. Shopify Balance and similar solutions exemplify banks powering merchant accounts natively.

Embedded Lending and Credit

Lending is embedded at purchase points or within business tools, offering instant decisions via API connections. Retailers and vertical SaaS platforms now provide “buy now, pay later” or working capital solutions backed by bank balance sheets.

Embedded Banking and Accounts

Through BaaS providers like Treasury Prime or Unit, banks offer white-label checking accounts, cards, and treasury tools inside gig economy apps, accounting software, or marketplaces. Users receive bank services without leaving the primary platform.

Key Benefits for Banks and Customers

For banks, embedded finance expands reach, diversifies revenue, and strengthens customer relationships without heavy front-end investment. Platforms gain new monetization while customers enjoy convenience and personalization.

- Reduced customer acquisition costs

- Higher conversion rates and basket sizes

- Real-time, data-driven personalization

- New revenue streams from partnerships

Real-World Examples in 2026

Major banks like JPMorgan, Goldman Sachs, and U.S. Bank power embedded solutions across retail, gig work, and B2B platforms. Shopify merchants access embedded banking services, while auto retailers offer instant financing powered by bank APIs.

In life-moment scenarios, home improvement platforms embed home equity lines, and HR systems offer embedded benefits and advances tailored to employee needs.

Challenges and Risks

Regulatory compliance, risk management, data privacy, and partnership complexities remain key hurdles. Banks must balance innovation with accountability as finance becomes “invisible.” Strong governance and technology are essential.

The Future of Embedded and Life-Moment Banking

By late 2026 and beyond, AI-driven insights, real-time payments, and deeper platform integrations will make finance even more contextual. Banks that excel as enablers or strategic partners will lead the next era of financial services.

Frequently Asked Questions

What is embedded finance?

Embedded finance integrates banking products like payments and lending directly into non-financial platforms, making financial services seamless and contextual.

What is life-moment banking?

Life-moment banking delivers financial solutions at key life events—such as buying a home or starting a business—within the platforms customers already use.

How are banks using embedded finance in 2026?

Banks partner with platforms via APIs and BaaS to offer embedded payments, lending, accounts, and insurance, expanding reach and creating new revenue streams.

What are the benefits of embedded finance?

Benefits include greater convenience for customers, expanded market reach for banks, higher conversion rates, and diversified revenue for all parties involved.

What platforms use embedded finance?

E-commerce sites like Shopify, gig economy apps, accounting software, HR platforms, and B2B marketplaces commonly embed financial services.

{kind=link}