Mastering how to save money fast is a practical skill that delivers immediate financial relief and long-term security, especially in an economy with persistent inflation and rising costs. By focusing on high-impact changes like expense tracking, automatic savings, and targeted cuts, individuals can accumulate hundreds or thousands in weeks or months without extreme deprivation.

This guide outlines proven, realistic methods tailored for 2026, including automation tools, challenge formats, and bill optimizations. Implement these steps consistently to see noticeable progress quickly while building sustainable habits.

Simple act of saving coins illustrates the power of consistent small deposits toward rapid financial growth.

Why Saving Money Quickly Matters in 2026

With everyday expenses remaining elevated, building savings buffers against unexpected costs like repairs or medical bills. Fast-saving approaches prioritize immediate cash flow improvements over long-term investments initially, creating momentum and reducing financial stress.

Realistic goals—such as $1,000 in an emergency fund within 3–6 months—are achievable for most through disciplined tracking and cuts. Automation and mindset shifts make the process effortless over time.

Step 1: Track Spending and Create a Realistic Budget

Understanding where money goes is the foundation of fast saving. Many overlook small daily leaks that add up significantly.

- Review the last 1–3 months of bank and credit card statements.

- Categorize expenses (essentials, wants, subscriptions, dining).

- Use the 50/30/20 rule as a starting point: 50% needs, 30% wants, 20% savings/debt.

- Adjust to identify $200–$500 monthly in reducible spending.

Example: A household discovers $150 monthly on unused subscriptions and $300 on takeout—cutting these frees $450 instantly for savings.

Visual budget dashboard helps track income, expenses, and progress toward fast savings goals.

Step 2: Automate Savings Transfers Immediately

Pay yourself first by moving money before spending temptation arises. This “out of sight, out of mind” tactic accelerates accumulation.

- Set up automatic transfers to a high-yield savings account on payday (even $50–$100 weekly adds up).

- Choose accounts offering 4%+ APY to grow funds faster through interest.

- Start small if needed—consistency compounds results.

Real-world impact: Transferring $100 bi-weekly builds over $2,600 annually, plus interest, providing a quick emergency buffer.

Step 3: Slash Recurring Bills and Subscriptions

Fixed costs offer some of the fastest wins—negotiate or eliminate them for instant monthly gains.

- Audit streaming, gym, app, and membership charges—cancel unused ones.

- Call providers (phone, internet, insurance) to negotiate lower rates or switch plans.

- Switch to generic brands for household items and shop sales/loyalty programs.

- Refinance high-interest debt if rates have dropped.

Example: Negotiating a $60 monthly phone bill reduction and canceling two $15 subscriptions saves $90 monthly—over $1,000 yearly redirected to savings.

External resource: For budgeting tools and high-yield account comparisons, visit NerdWallet’s savings guide.

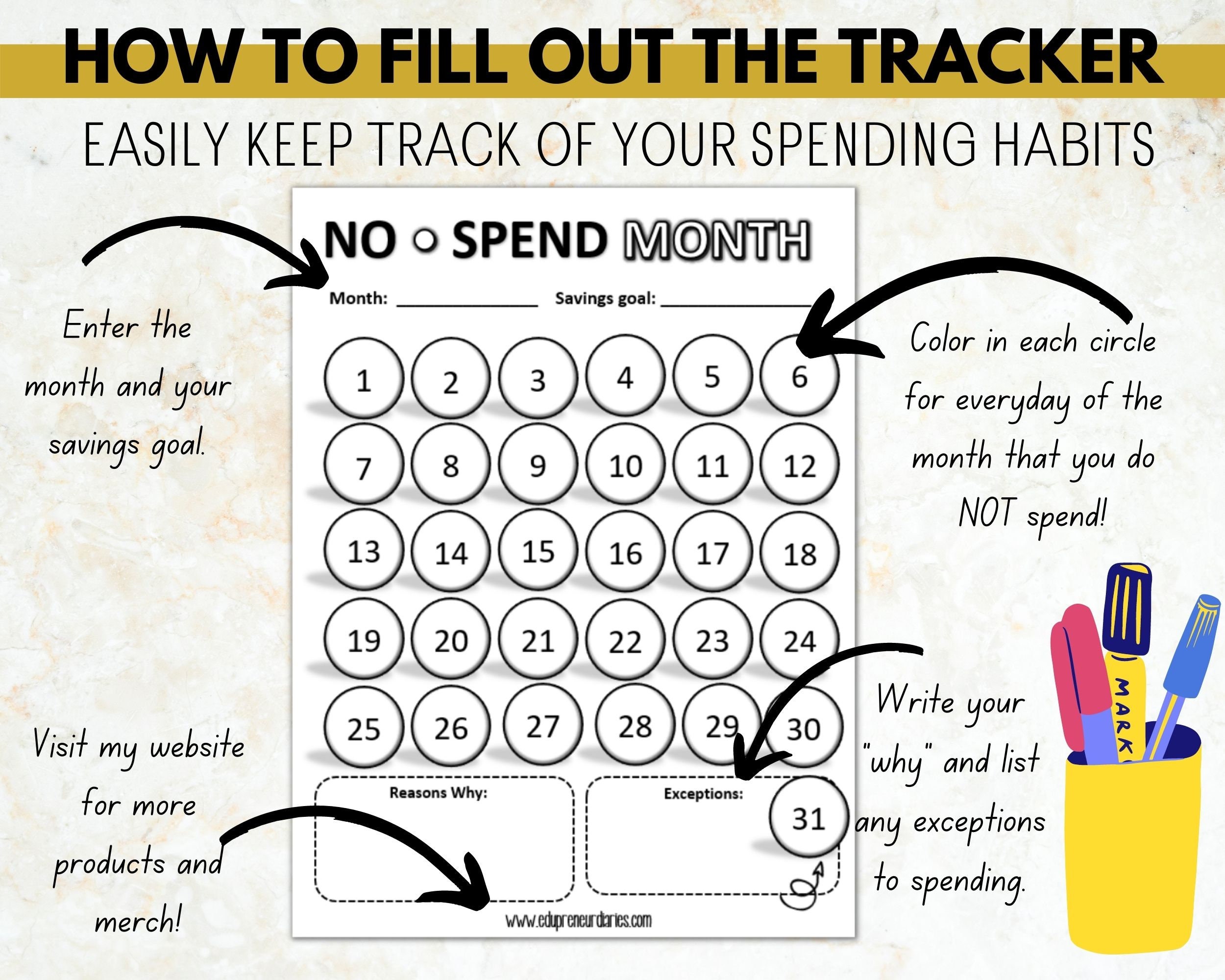

Step 4: Implement No-Spend Challenges and Spending Freezes

Short-term restrictions create rapid momentum by forcing mindful habits.

- Try a 30-day no-spend month on non-essentials (track days without purchases).

- Do weekly no-spend days or “free weekends” using home activities.

- Use visual trackers (printable calendars or apps) to mark progress and stay motivated.

A participant in a no-spend January challenge saves $800 by avoiding dining out and impulse buys, building both funds and discipline quickly.

No-spend tracker encourages accountability and visual progress in fast-saving efforts.

Step 5: Optimize Grocery and Everyday Spending

Food and household costs are flexible areas for quick reductions.

- Plan meals weekly, shop with lists, and prep to avoid waste and delivery fees.

- Buy in bulk for staples, choose store brands, and use cashback apps.

- Limit eating out to once weekly or less—cook at home for significant savings.

- Try “meatless” or low-cost ingredient days.

Example: Meal planning cuts a $600 monthly grocery bill to $400, freeing $200 monthly for savings.

Step 6: Build an Emergency Fund as Priority

Aim for $1,000–$3,000 quickly as a safety net, then expand to 3–6 months’ expenses.

- Direct windfalls (tax refunds, bonuses) entirely to savings.

- Sell unused items online for one-time boosts.

- Use high-yield accounts to earn while saving.

Many achieve $1,000 in 2–4 months by combining cuts and automation, reducing reliance on credit during surprises.

External resource: Review emergency fund strategies at Investopedia.

Additional Fast-Saving Tips for 2026

Use cashback/rewards cards responsibly (pay in full monthly). Energy audits lower utility bills—switch to LED bulbs and unplug devices. Walk or use public transit to cut fuel costs. Review insurance annually for better rates.

Avoid lifestyle inflation from raises—channel increases to savings. Track progress monthly to maintain motivation and adjust tactics.

For U.S. self-employment tax considerations on side income used for savings, see IRS guidelines.

Frequently Asked Questions

How can I save $1,000 fast realistically?

Combine automatic transfers ($100+ bi-weekly), cut subscriptions/dining ($200–$300 monthly), and sell unused items. Many reach $1,000 in 2–4 months with focused effort.

What is the quickest way to start saving money fast?

Track spending for one week, cancel unused subscriptions immediately, and set up an automatic transfer to a high-yield savings account on payday—even small amounts build momentum quickly.

Can I save money fast without a high income?

Yes—focus on reducing variable expenses like food and entertainment. Meal planning, no-spend challenges, and bill negotiations work regardless of income level.

Are no-spend challenges effective for fast savings?

Highly effective for short bursts—they curb impulse spending and highlight habits. A 30-day challenge often saves hundreds by limiting non-essential outflows.

How do high-yield savings accounts help save faster?

They earn 4%+ interest annually, adding extra growth without effort. Pairing them with automatic deposits accelerates balance increases compared to standard accounts.

What common mistakes slow down fast saving?

Ignoring small recurring charges, not tracking progress, or dipping into savings for non-emergencies. Consistency and review prevent setbacks.

{kind=link}